Water Damage Insurance Claims Guide: How to Document Damage and Protect Your Claim

You step into the hallway and feel water under your feet. A supply line has failed, the ceiling has started dripping, or an appliance has leaked overnight. Your first thought may be about the repair bill. However, the actions you take during the first few hours can affect both the property and your insurance claim. Calling a local provider of water mitigation restoration in Austin can help stop the spread while you begin documenting the loss.

Water damage claims often involve several parties. You may speak with an insurance representative, adjuster, plumber, restoration contractor, and mortgage company. Keeping clear records can make those conversations easier. It can also help you explain when the damage started, what caused it, and what work became necessary.

Stop the Water and Protect the Property

Safety comes first. Turn off the main water supply when the leak comes from plumbing or an appliance. Do not enter rooms with standing water near outlets, electrical panels, or exposed wiring. Contact emergency services or an electrician when you suspect an electrical risk.

You should also take reasonable steps to prevent the damage from getting worse. Home insurance policies commonly require policyholders to protect damaged property after a loss. This may include stopping the water source, moving dry belongings away, placing containers under active leaks, or arranging temporary repairs. Policies may cover sudden and accidental plumbing discharges, but coverage depends on the cause, maintenance history, exclusions, and policy wording.

Do not begin major demolition before speaking with your insurance company unless waiting would create a safety risk or allow more damage. Emergency water extraction and drying may need to start quickly. Ask the restoration company to photograph affected areas before removing wet materials.

Keep damaged items unless they create a health or safety concern. Separate wet belongings from undamaged property when possible. Your adjuster may want to inspect them. If something must be discarded, photograph it clearly before removal and record its brand, age, condition, and approximate value. FEMA also advises property owners to save repair receipts and keep damaged items separate for inspection when possible.

Document Every Part of the Water Damage

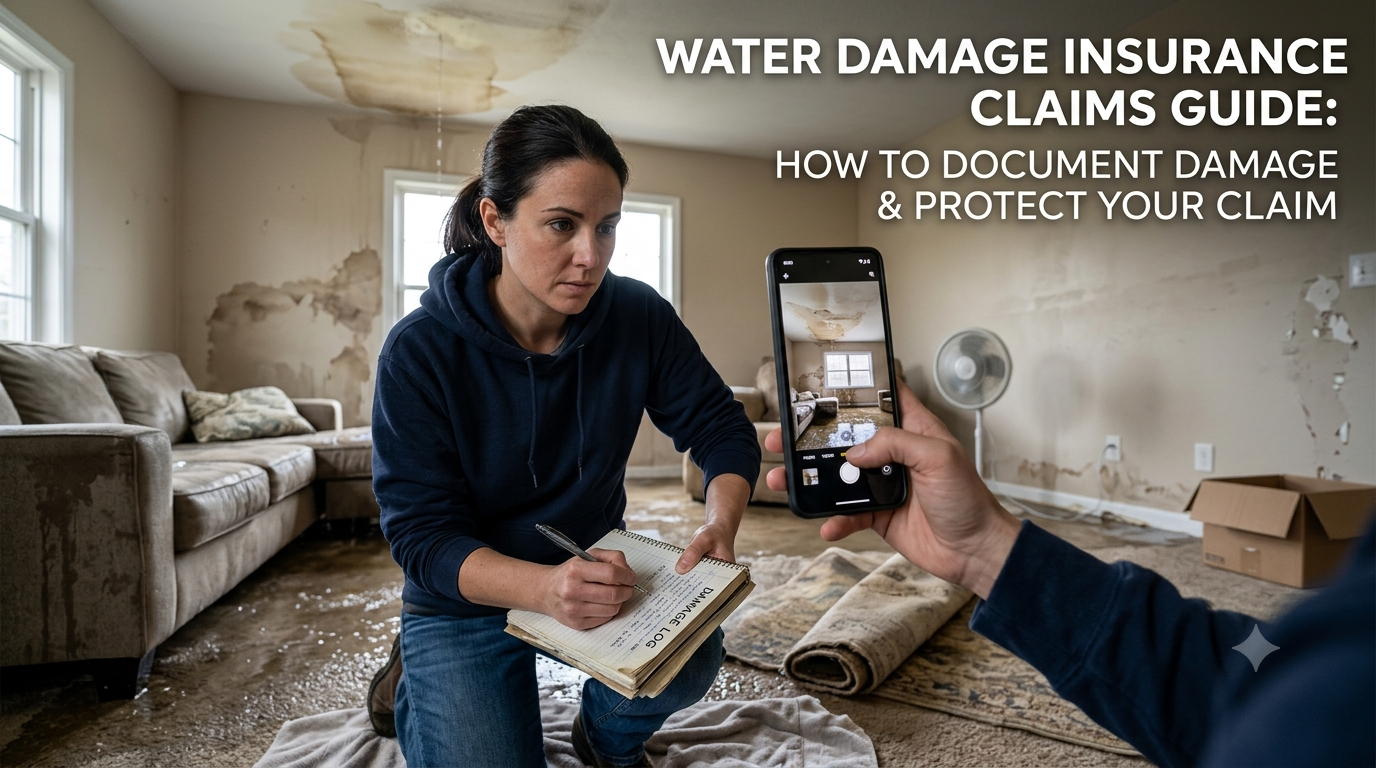

Strong documentation tells the story of the loss. Start taking photographs and videos as soon as the area becomes safe. Capture wide views of each room before taking close photographs of damaged walls, floors, ceilings, cabinets, furniture, and personal belongings.

Photograph the suspected source. This could include a burst pipe, broken supply line, overflowing fixture, leaking water heater, damaged roof section, or failed appliance connection. Do not claim that you know the exact cause unless a qualified professional has confirmed it.

Create a written timeline that includes:

-

When you first noticed the water

-

Where the water appeared

-

When you shut off the supply

-

Who you called for help

-

What emergency work took place

-

Which rooms and belongings suffered damage

-

Every conversation with the insurance company

Save emails, text messages, claim forms, estimates, invoices, receipts, and inspection reports. Keep digital copies in a cloud folder or email them to yourself. Paper records can become damaged during cleanup.

Make a detailed inventory of affected belongings. Include product names, model numbers, purchase dates, original costs, and replacement prices when available. Receipts, credit card statements, online order histories, and old photographs may help prove ownership.

Photographs and videos should show structural damage, damaged contents, and the water level when visible. Detailed records help the insurer and adjuster understand the scope of the loss. FEMA recommends photographing damaged property and retaining expense receipts during an insurance claim.

Contact Your Insurer and Understand the Coverage

Report the loss as soon as reasonably possible. Ask the insurance company for your claim number and the adjuster’s contact information. Write down the date, time, representative’s name, and a summary of every call.

Ask direct questions about:

-

Your deductible

-

Emergency mitigation coverage

-

Temporary repair approval

-

Personal property coverage

-

Additional living expenses

-

Replacement cost or actual cash value

-

Required estimates and inspections

-

Deadlines for submitting documents

A deductible is the amount you generally pay before covered insurance benefits apply. Reviewing it can help you compare the likely repair cost with the value of filing a claim. Reporting deadlines and claim procedures may differ by state and insurer.

Coverage also depends heavily on how the water entered the property. Standard homeowners insurance often treats a sudden plumbing leak differently from groundwater flooding, storm surge, long-term seepage, poor maintenance, or sewer backup. Standard homeowners policies usually do not cover outside flooding. Flood losses generally require separate flood insurance. Sewer or drain backup may also require an endorsement.

Do not assume that visible water marks show the full damage. Moisture can move behind drywall, under flooring, through insulation, and inside cabinets. Ask the restoration contractor to provide moisture readings, photographs, drying logs, equipment records, and a written scope of work. These records may help support the work performed.

Work Carefully With the Adjuster and Contractors

The insurance adjuster will review the damage, policy terms, documentation, and repair estimates. Be honest and specific. Do not exaggerate the loss, guess about facts, or throw away evidence without recording it.

Walk through every affected area with the adjuster. Point out staining, swelling, odors, loose flooring, damaged trim, wet insulation, and affected personal property. Ask whether the adjuster needs additional photographs, estimates, or proof of ownership.

You may obtain your own contractor estimates. Compare each scope carefully. One estimate may include only visible repairs, while another includes drying, material removal, cleaning, rebuilding, and painting. A low estimate may leave out necessary work.

Read every document before signing it. Understand whether you are authorizing emergency services, full reconstruction, direct insurance billing, or an assignment of benefits. Laws and contract rules vary, so request legal advice when you do not understand a document.

If a mortgage exists, the insurer may issue the settlement check to both you and the mortgage servicer. The servicer may release the funds in stages as repairs progress. Contact the mortgage company early so you understand its inspection and payment process.

Avoid Mistakes That Can Weaken a Claim

Many claim problems start with missing records or delayed action. Homeowners sometimes clean everything before taking photographs. Others approve repairs without getting written estimates or fail to keep hotel and meal receipts.

Avoid these common mistakes:

-

Waiting too long to report the damage

-

Ignoring an active leak

-

Discarding items without photographs

-

Making permanent repairs before inspection

-

Giving uncertain answers as confirmed facts

-

Losing receipts and drying records

-

Accepting a settlement without reviewing the scope

-

Assuming every type of water damage receives coverage

If the home becomes unlivable after a covered loss, the policy may include additional living expense coverage. This coverage may help with temporary housing and certain extra costs. Keep itemized receipts and ask the insurer which expenses qualify before making large commitments.

Take the Next Step With a Clear Record

A water damage claim becomes easier to manage when you control the source, protect the property, document the loss, and communicate in writing. Keep your claim number, photographs, inventory, estimates, receipts, and adjuster notes together. Review your policy and ask questions whenever an instruction seems unclear.

Insurance coverage always depends on the policy, cause of damage, and claim findings. This guide provides general information and does not replace legal or insurance advice.

Fast drying can help limit further property damage while creating a clear record of the affected areas. For professional emergency water removal in Austin TX, contact Legacy Water Restoration. The team can inspect the damage, remove standing water, document affected materials, and begin the drying process. Call Legacy Water Restoration promptly so your home and insurance records receive careful attention from the beginning.